Calculating College Costs

The Price Tag Is a Fiction: How College Costs Really Work

Every fall, families open college websites, scroll to the tuition page, and experience the same visceral reaction: sticker shock. A private university lists a total cost of attendance north of $80,000. An out-of-state public school comes in at $50,000. Even in-state flagship universities have crossed the $30,000 mark when room, board, and fees are included. The numbers feel impossible, and for many families, they trigger one of two responses—either panic or premature elimination of schools that might actually be affordable.

Both responses are mistakes, because the listed cost of attendance at most colleges is a fiction. It is the sticker price on a car that no one is expected to pay. The real number—what families actually write checks for—is often dramatically lower, and it varies wildly depending on the family’s income, the student’s academic profile, and the specific financial aid policies of each institution. Understanding how this system works is not optional for families navigating the college planning process. It is the single most important piece of financial literacy they will need in their college planning journey.

Almost Nobody Pays the Sticker Price

The gap between what colleges advertise and what students actually pay is enormous. According to the College Board’s 2025 Trends in College Pricing report, the average published tuition and fees at private nonprofit four-year institutions reached $45,000 for the 2025–26 academic year. But the average net tuition and fees—the amount students actually paid after grants and scholarships—was approximately $16,910. That means the typical student at a private college received nearly $28,000 in grant aid that did not need to be repaid.

The pattern is even more striking at public universities. The average published in-state tuition and fees at public four-year institutions was $11,950 in 2025–26. But after accounting for grant aid, the average net tuition and fees for first-time, full-time in-state students dropped to an estimated $2,300. That is not a typo. The typical in-state student at a public four-year college paid roughly $2,300 in tuition and fees out of pocket after financial aid.

These averages mask significant variation—a family earning $200,000 per year will pay considerably more than a family earning $60,000—but the central point holds. The published cost of attendance is not what most families pay, and dismissing a school based solely on its sticker price is one of the most common and costly errors families make in the college search process.

How Need-Based Aid Works: The Formula Behind the Number

Need-based financial aid is built on a straightforward formula: a college’s total cost of attendance minus the family’s demonstrated ability to pay equals the student’s financial need. The college then decides how much of that need to meet with grants, scholarships, work-study, and loans.

The family’s ability to pay is determined by a standardized calculation. At the federal level, this is done through the FAFSA—the Free Application for Federal Student Aid—which produces a number called the Student Aid Index, or SAI. The SAI replaced the older Expected Family Contribution (EFC) as part of the FAFSA Simplification Act, and it functions as a snapshot of what the federal formula believes a family can contribute toward college in a given year. It is calculated based on household income, assets, family size, and certain other factors. Importantly, the SAI can now go as low as negative $1,500, meaning some families are identified as having need that exceeds even the full cost of attendance.

About 250 private colleges use an additional form called the CSS Profile, administered by the College Board, which collects more detailed financial information than the FAFSA. The CSS Profile considers factors the FAFSA ignores, such as home equity, non-custodial parent income in divorce situations, and certain business assets. Schools that use the CSS Profile calculate their own institutional SAI, which may differ significantly from the federal number. This means the same family can have two different “ability to pay” figures depending on which form a school uses—and that difference can translate into thousands of dollars in aid.

Here is where it gets critical: just because a college calculates your financial need does not mean the college will meet all of it. The formula determines eligibility. The college’s own budget and aid policies determine the actual award.

Not All Colleges Meet Your Full Need—And Most Don’t

This is the part of the financial aid process that catches families off guard. Only a small fraction of American colleges—roughly 75 institutions—commit to meeting 100 percent of every admitted student’s demonstrated financial need. These tend to be the wealthiest and most selective schools in the country: the Ivy League, Stanford, MIT, a handful of elite liberal arts colleges, and a few well-endowed state universities. Their enormous endowments allow them to guarantee that no student will face a gap between what the formula says they need and what the school provides.

The remaining several thousand colleges and universities in the United States operate differently. Most of them practice what financial aid professionals call “gapping”—they calculate your demonstrated need and then meet only a portion of it. A family might have a calculated need of $30,000 at a particular school, but the school’s aid package covers only $20,000. The remaining $10,000 is the gap, and the family is expected to cover it through additional borrowing, outside scholarships, or out-of-pocket payment.

The size of the gap varies enormously from school to school. A well-resourced state university might meet 85 percent of need. A mid-tier private college with a smaller endowment might meet only 60 or 70 percent. Some schools fill the gap primarily with grants, while others rely heavily on loans that must be repaid, which technically count as “aid” in the award letter but are nothing like free money. This is why comparing financial aid offers requires reading the fine print—a $35,000 aid package that includes $15,000 in loans is a fundamentally different proposition from a $30,000 package that is entirely grants.

How Merit Aid Changes the Equation

Need-based aid is only one half of the financial aid picture. The other half—and for many middle-class families, the more consequential half—is merit-based aid. Merit scholarships are awarded based on a student’s academic profile, not the family’s financial situation. A student does not need to demonstrate need to receive merit aid; they need to demonstrate achievement.

Merit aid is where a student’s GPA and test scores translate directly into money, and the amounts can be substantial. More than half of institutional merit scholarships go to students with a 3.5 GPA or higher on an unweighted 4.0 scale. At many schools, strong test scores can be worth tens of thousands of dollars per year. One analysis found that at certain institutions, a single additional point on the ACT—or the equivalent ten-point increase on the SAT—was worth $25,000 over four years.

But here is the piece that most families miss: merit aid is not distributed uniformly across all schools. It is a strategic tool that colleges use to attract students who will raise the institution’s academic profile. A student with a 1350 SAT score will likely receive little or no merit aid from a school whose admitted students average 1400. But that same student might receive $15,000 to $25,000 per year from a school whose average admitted SAT is 1200, because at that school, the student is a statistical asset the institution wants to recruit.

This creates a powerful strategic dynamic. A student who applies exclusively to reach schools—schools where their academic profile is at or below the median—is unlikely to receive meaningful merit aid from any of them. A student who includes schools where their profile is in the top 25 percent of the admitted class is far more likely to receive a significant merit scholarship. The practical difference can be $60,000, $80,000, or even $100,000 over four years. For families who do not qualify for substantial need-based aid, merit aid is often the single largest lever available to reduce college costs, and the schools on the student’s list determine whether that lever gets pulled.

Three Schools, Three Very Different Price Tags

To see how all of this works in practice, consider a hypothetical family: household income of $110,000, one student heading to college, modest savings. The student has a 3.7 GPA and a 1320 SAT score. Here is what might happen at three different types of institutions.

Scenario One: High-Endowment Private University. The sticker price is $82,000 per year. The school uses the CSS Profile and meets 100 percent of demonstrated need. The institutional formula determines the family can contribute $28,000 per year. The school covers the remaining $54,000 entirely with institutional grants. The student’s annual out-of-pocket cost: $28,000. No merit aid is offered because the student’s test scores are below the school’s median, and the school is selective enough that it does not need to use merit money to attract applicants.

Scenario Two: State Flagship University (In-State). The cost of attendance is $28,000 per year. The FAFSA determines the family’s SAI is $22,000. The school meets approximately 70 percent of the student’s $6,000 in calculated need, providing $4,200 in grants. But the student’s academic profile places them in the top 20 percent of the incoming class, which qualifies them for a $6,000 annual merit scholarship. Combined, the student receives $10,200 in aid. Annual out-of-pocket cost: approximately $17,800.

Scenario Three: Mid-Tier Private College. The sticker price is $58,000 per year. The school uses only the FAFSA and meets about 65 percent of demonstrated need. The family’s calculated need is $36,000, and the school provides $23,400 in need-based grants. But the student’s 1320 SAT and 3.7 GPA place them well above the school’s median academic profile, earning an additional $18,000 annual merit scholarship. Total aid: $41,400. Annual out-of-pocket cost: approximately $16,600.

Notice what happened. The school with the highest sticker price did not end up being the most expensive option. The mid-tier private school, which might have been dismissed on sight because of its $58,000 price tag, actually produced the lowest net cost because the combination of need-based and merit-based aid was so favorable. This is exactly the kind of outcome families miss when they eliminate schools based on sticker price alone. Everyone’s situation will be different. That means everyone’s best financial fits are different too. It is critical that you understand which school are the best fit for YOU!

The Tools That Make This Calculable

Families do not need to guess at these numbers. Federal law requires every college that participates in federal financial aid programs to provide a Net Price Calculator on its website. These calculators allow families to enter their income, asset, and household information and receive an estimate of what students with similar financial profiles actually paid to attend. The estimates are not binding offers, but they are grounded in real institutional data and provide a far more accurate picture of cost than the published price tag. However, you need to be careful. Net Price Calculators are required to exist but they are not required to be up to date and accurate. Typically, the fewer questions you are asked, the less accurate it is.

For federal aid, the FAFSA itself offers an estimator tool at studentaid.gov that helps families understand their likely SAI before they file. This is useful for early planning, especially for families of high school juniors who want to start building a financially informed college list well before application season.

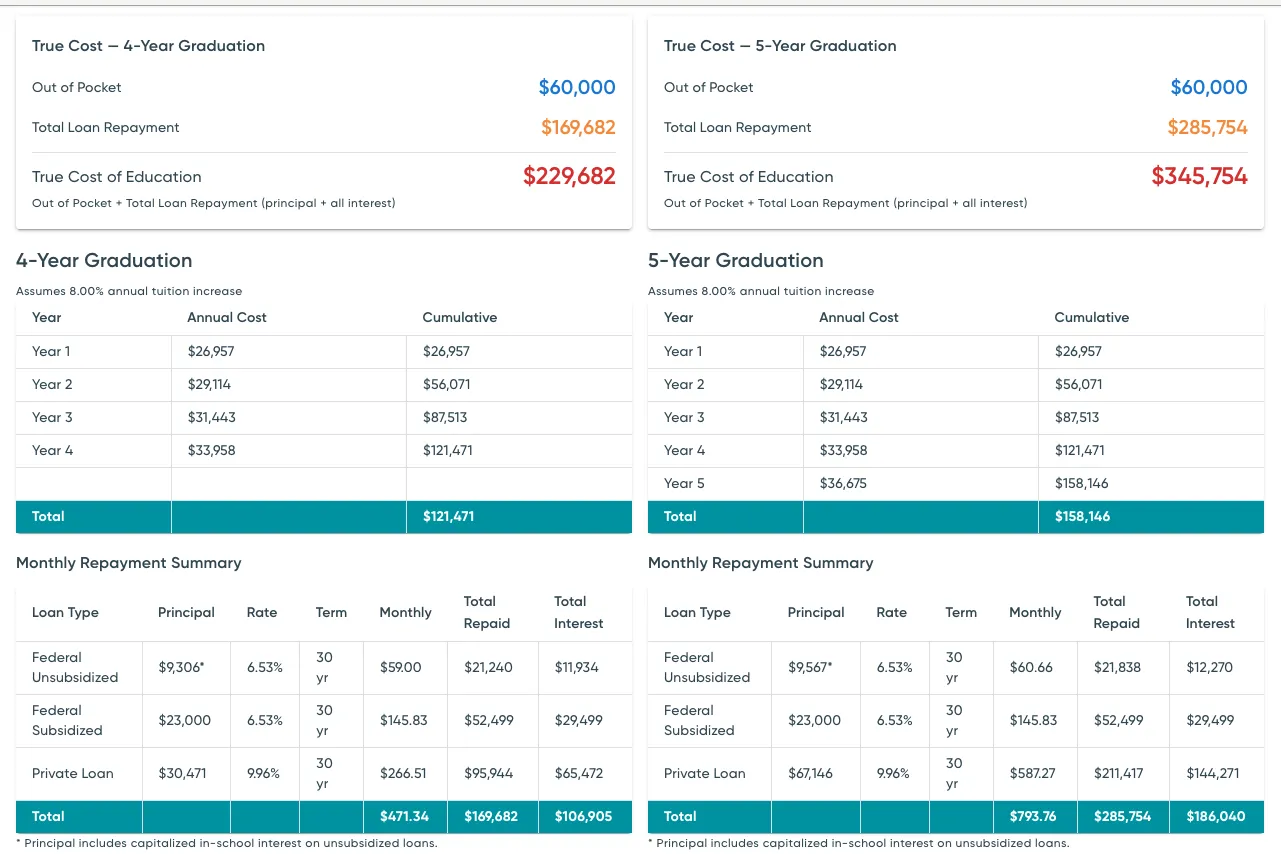

Guided’s platform has all the actual scholarship data, need-based aid, and merit-based aid tools you need to properly evaluate the cost of a college for you. Proper planning is crucial to getting the best outcomes. Our True Cost of Education and Life Simulation calculators let you run different scenarios at different colleges based on your family’s savings to see what your debt would be and how it will impact your future when you graduate.

The strategic move is to run the Net Price Calculator at every school on the student’s list before finalizing applications. This takes time, but the payoff is enormous. It transforms the college search from a process driven by reputation and guesswork into one driven by real financial data. Families who do this work early consistently make better decisions and avoid the painful surprise of an unaffordable aid package arriving in April of senior year.

Building a College List That Matches Your Financial Reality

The most important financial decision in the college process is not choosing between schools after admission—it is choosing which schools to apply to in the first place. A strategically built college list takes into account not just academic fit and campus culture but the financial profile of each institution and the student’s positioning within it.

Families should be looking at three things for every school on the list. First, does the school meet full demonstrated need, and if not, what percentage does it typically meet? Second, does the school offer merit-based aid, and where does the student’s academic profile fall relative to the school’s admitted student averages? If the student is at or above the 75th percentile for GPA and test scores, that school is likely to offer meaningful merit money. Third, what does the Net Price Calculator say for a family with your financial profile? Again, all of the tools you need are available through our platform.

A well-built list will include a mix of schools: some where the student is likely to receive strong merit aid because their profile exceeds the school’s median, some where need-based aid policies are generous enough to make the school affordable despite a higher sticker price, and ideally at least one or two financial safety schools where the combination of low cost and available aid makes the school affordable under virtually any scenario.

This approach requires families to set aside ego and prestige and focus on outcomes. The school that offers a student a $20,000 annual merit scholarship because they are in the top quarter of the class is not a lesser school—it is a school that is investing in that student. And the financial freedom that comes from graduating with little or no debt is worth far more than the marginal difference in name recognition between two institutions.

The Bottom Line

College pricing is a system that rewards informed families and penalizes those who accept the sticker price at face value. The published cost of attendance is a starting point for negotiation, not a final answer. Need-based aid, merit-based aid, and institutional financial policies create a landscape where two families sitting next to each other in the same freshman orientation may be paying wildly different amounts for the same education.

The families who come out ahead are the ones who do the math before they fall in love with a campus. They run the Net Price Calculators. They understand the difference between the FAFSA and the CSS Profile. They build college lists that align their student’s academic strengths with institutions that will reward those strengths financially. They treat the college search not just as an academic decision but as one of the largest financial decisions their family will make—because that is exactly what it is.

Ready to take the next step?

Get personalized guidance for your career and college planning journey.