Why Income Based Repayment Plans Are More Likely To Bury You In Debt

Income-Based Repayment plans are NOT the answer. Better planning is.

Income-based repayment plans are marketed as a lifeline. If your student loan payments are too high relative to your earnings, the federal government will cap your monthly payment at a percentage of your discretionary income. The pitch sounds compassionate and practical: pay what you can afford, and after twenty or twenty-five years, maybe part or all the remaining balance is forgiven. Maybe. For a borrower staring at a loan payment they cannot make, it feels like the system is working in their favor.

But behind that reassuring framework is a mathematical reality that most borrowers do not understand until they are years into the plan and watching their balance climb. When your monthly payment does not cover the interest accruing on your loan, the unpaid interest is added to your principal. Your balance does not shrink. It grows. You are making payments every single month and going deeper into debt at the same time. This is not a theoretical edge case. It is the lived experience of millions of American borrowers, and it is one of the least discussed financial crises in higher education today.

How Income-Based Repayment Actually Works

Income-driven repayment plans—including IBR, PAYE, and the soon-to-be killed SAVE plan—calculate your monthly payment based on a formula tied to your income, not your loan balance. The standard formula takes your adjusted gross income, subtracts 150 percent of the federal poverty guideline for your family size, and then sets your payment at 10 to 15 percent of the remaining amount, divided by twelve. For a single borrower earning $40,000, this calculation can produce a monthly payment that is a fraction of what the standard repayment plan would require.

The problem is that interest does not care about your income. Interest is calculated based on your loan balance and your interest rate, period. If you owe $60,000 at 8.5 percent interest—a realistic blended rate for a borrower with a combination of federal and private loans—your loan generates $425 in interest every single month. If your income-based payment is set at $240 per month, you are paying $185 less than the interest alone. That $185 gets added to your balance. Next month, interest is calculated on the new, higher balance, which means even more unpaid interest gets capitalized. The cycle compounds month after month, year after year.

In accounting, this phenomenon has a name: negative amortization. It means your debt is growing even though you are making payments. And for borrowers on income-based plans whose payments fall below their monthly interest, it is not a bug in the system. It is how the system is designed to work.

The Numbers: What Happens to a $60,000 Loan Under IBR

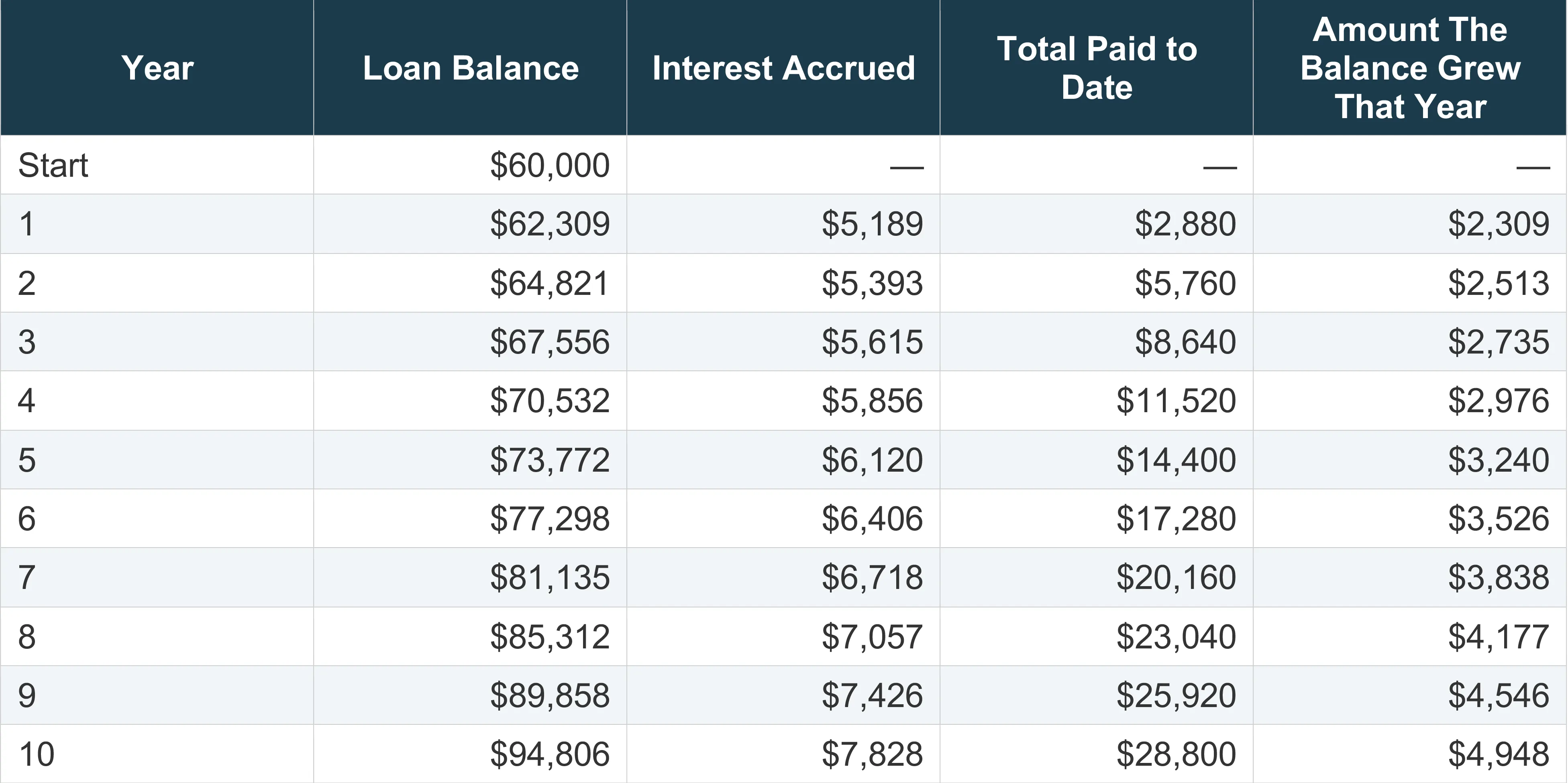

Let us trace the math with a concrete example. A borrower graduates with $60,000 in student loan debt at a blended interest rate of 8.5 percent. Under a standard 30-year repayment plan, their monthly payment would be $461.35. But their income qualifies them for an income-based repayment of just $240 per month—a reduction that feels like a relief. The borrower is saving $221.35 per month compared to the standard payment. Except they are not saving anything. They are deferring it, with interest.

Here is what happens to that borrower’s balance over ten years of $240 monthly IBR payments:

Read that final row carefully. After ten years of faithful monthly payments—120 consecutive payments totaling $28,800—the borrower does not owe $60,000. They owe $94,806. Their balance has grown by nearly $35,000. They have paid almost $29,000 and are deeper in debt than the day they graduated. The total interest that accrued over those ten years was $63,606—more than the original loan itself—and the $240 monthly payment covered less than half of it. Don’t forget, that’s with a 10 year repayemnt. If that IRB plan was amortized over 25 years, like many are, the student loan debt grows way bigger.

The 10-Year Amortization Scenario: An Even Starker Picture

Now consider a borrower with the same $60,000 loan at 8.5 percent, but this time amortized over a standard 10-year repayment term. The required monthly payment under this plan is $743.91. If this borrower had made those payments faithfully for ten years, they would have paid off the loan in full. The debt would be gone.

Instead, the borrower enrolls in income-based repayment at $240 per month. The monthly shortfall compared to the standard 10-year payment is a staggering $503.91. And because the underlying loan balance and interest rate are the same, the negative amortization is identical: the balance still grows to $94,806 after ten years. But the opportunity cost is dramatically different. Here is what the borrower’s financial position looks like under each scenario after ten years:

The borrower who chose the standard 10-year plan is debt-free. The borrower who chose the standard 30-year plan still owes $53,161 but has been steadily reducing the balance. The borrower on income-based repayment has paid the least amount of money out of pocket—and owes the most. They owe nearly $35,000 more than they originally borrowed and $42,000 more than the 30-year borrower. The lower monthly payment did not save them money. It cost them a fortune.

The Snowball Effect: Why It Gets Worse, Not Better

What makes negative amortization so destructive is that it accelerates over time. In year one, the borrower’s $240 monthly payment fails to cover the interest, and roughly $2,309 is added to the balance. By year five, the balance has grown enough that the annual interest shortfall adds $3,240. By year ten, the annual shortfall has more than doubled to $4,948. The balance is not just growing—it is growing faster each year because interest is being charged on previously unpaid interest.

This is the same compounding mechanism that makes savings accounts and investment portfolios grow over time—except it is working against the borrower instead of for them. Every dollar of unpaid interest becomes part of the new principal, which generates its own interest the following month. It is a debt snowball rolling downhill, and the longer it rolls, the faster it accelerates.

For borrowers who remain on income-based repayment for the full twenty or twenty-five year term, the final balance can be staggering. A borrower who started with $60,000 can easily see their balance exceed $150,000 or more before the forgiveness window opens—all while having made consistent monthly payments the entire time.

If forgiveness does not happen, which sadly is common, the borrower just demolished their financial future with no way out other than paying. Student loans are there until you pay them off. Not even filing for bankruptcy clears them off.

The Psychological Trap: Affordable Payments That Aren’t Affordable

Income-based repayment plans create a dangerous illusion of affordability. The borrower sees a lower monthly number, feels relief, and moves on with their life. They may not check their loan balance for years. When they finally do, the number is larger than they remember—sometimes much larger—and the realization is devastating. They have been paying their loans. They have been responsible. Now they are significantly further from financial freedom than the day they started.

This psychological dimension is not trivial. Research consistently shows that student loan debt is associated with higher rates of anxiety, delayed homeownership, postponed marriage and family formation, and reduced retirement savings. When a borrower discovers that years of payments have actually increased their debt, the psychological toll compounds the financial one. The feeling of being trapped—of running on a treadmill that is actually moving backward—is one of the defining financial experiences of an entire generation of college graduates.

What Borrowers Should Understand Before Enrolling

None of this means that income-based repayment is always the wrong choice. For borrowers in genuine financial hardship—those who cannot make any higher payment without sacrificing basic needs—IBR can prevent default and protect credit scores while the borrower works toward higher income. For borrowers pursuing Public Service Loan Forgiveness, which offers tax-free forgiveness after ten years of qualifying payments, IBR can be a rational strategy. However, Public Service Loan Forgiveness (PSLF), has faced significant scrutiny over its exceptionally complex process to qualify. Not to mention the fact that a significant portion of borrowers who did qualify were denied forgiveness regardless. Here’s some PSLF facts that will make you think. 5.48% of applications for Public Service Loan Forgiveness (PSLF) are approved. As bad as you think that number is, prior to a review ordered in 2021, that number was .03%. Not a typo. Of those who enroll in PSLF, just 18.4% of eligible student borrowers apply for loan forgiveness. Frequently, they miss out because they missed a step or more in the process over the ten years it takes to become eligible.

But for the average borrower who enrolls in IBR simply because the lower payment is more comfortable, the long-term cost is enormous. Before choosing an income-based plan, every borrower should answer three questions honestly. First, is my IBR payment enough to cover at least the monthly interest on my loan? If the answer is no, negative amortization will begin immediately. Second, do I have a realistic plan to increase my income to a level where I can eventually switch to standard payments or pay extra? If not, the balance will continue to grow for years or decades. Third, have I calculated the total amount I will pay over the life of the plan, including the inflated balance, compared to what I would pay under a standard repayment schedule?

The answers to these questions are often sobering. But they are far less painful to confront at the beginning of the repayment journey than ten years in, when $28,800 in payments has turned a $60,000 loan into a $95,000 one. Use Guided’s True Cost of Education calculator to examine the different scenarios you are considering using real college cost and debt data based off of your personal situation.

The Bigger Lesson: Borrow Less in the First Place

The most effective defense against the income-based repayment trap is not a better repayment strategy—it is borrowing less to begin with. A student who graduates with $20,000 in debt instead of $60,000 has a standard 10-year payment they can actually make on an entry-level salary. They never need to enroll in IBR. They never experience negative amortization. They pay their loan off in a decade and move on with their financial life.

This is why the college selection process matters so much. Choosing a school where merit and need-based aid minimize borrowing, attending a community college for the first two years, selecting an in-state public university over a more expensive private one—these decisions do not just affect the college experience. They determine whether a graduate enters the workforce with manageable debt or with a financial burden that an income-based repayment plan will quietly transform into a crisis.

The Bottom Line

Income-based repayment plans offer lower monthly payments. That is true. But lower monthly payments are not the same as lower total cost, and for borrowers whose payments fall below their monthly interest, the cost is not just higher—it is dramatically, compounding, relentlessly higher. A borrower who pays $240 per month on a $60,000 loan at 8.5 percent will owe nearly $95,000 after ten years of payments. They will have paid $28,800 and gotten $35,000 deeper into debt for the trouble.

The math is not complicated. But it is hidden behind language designed to make borrowers feel comfortable—words like “affordable,” “income-driven,” and “forgiveness.” The borrowers who fare best in this system are the ones who look past the language and read the numbers. And the numbers say this: if your monthly payment is not covering your interest, you are not repaying your loan. You are feeding it.

Ready to take the next step?

Get personalized guidance for your career and college planning journey.